If therapy is covered by insurance, why does it still cost $200 a session?

This is the question almost everyone asks — usually not before starting therapy, but after the first bill hits. You walk in expecting support from your insurance plan and walk out realizing you’re effectively paying full price, at least for now.

The confusion isn’t accidental. Insurance technically covers therapy, but the way that coverage is structured delays the benefit until you’ve already paid a significant amount out of pocket due to your deductible. By the time insurance starts helping in a meaningful way, many people have already started questioning whether they can afford to continue.

Understanding why this happens requires looking past the surface-level definitions of copays, coinsurance, and deductibles and instead focusing on how they actually play out over time.

The Hidden Timeline of Therapy Costs

Most explanations of insurance focus on definitions. The real issue is sequencing.

Therapy costs don’t stay constant — they evolve over time depending on where you are relative to your deductible. Early sessions are the most expensive, even though that’s when consistency matters most.

Take a common scenario. Someone starts therapy with a plan that includes a $1,500 deductible, which is close to the average health insurance deductible in the U.S. and 30% coinsurance. They find a therapist who charges $200 per session, which aligns with the average cost of therapy in the U.S. and which is typical for out-of-network care.

For the first several weeks, nothing is shared with insurance. Each session is paid entirely out of pocket, and every payment simply moves them closer to their deductible. There’s no visible benefit yet, just accumulation. By the time they reach session six or seven, they’ve likely spent over $1,200. This is the point where the financial pressure starts to compete with the therapeutic progress. It’s also where many people begin spacing out sessions or stopping altogether.

Only after crossing the deductible does the structure change. At that point, the same $200 session might effectively cost $60, with insurance covering the rest. The service hasn’t changed, but the affordability suddenly has.

The problem is that the system makes you experience the most expensive version of therapy first and the most affordable version later.

Why the System Feels Misleading (Even When It Isn’t)

From a technical standpoint, nothing is hidden. Deductibles, coinsurance rates, and reimbursement policies are all documented. But the way they interact creates an experience that feels very different from what people expect when they hear “covered by insurance.”

Coverage suggests immediate cost reduction. But in reality, cost remains one of the primary barriers to care, as shown in research on cost as a barrier to therapy. In practice, coverage often means delayed participation.

This gap between expectation and reality is what creates friction. People don’t abandon therapy because they misunderstand definitions — they abandon it because the early financial burden is misaligned with how care actually works.

Mental health care is not episodic. It requires consistency, especially in the early stages. A system that front-loads cost into that exact period introduces risk at the worst possible moment.

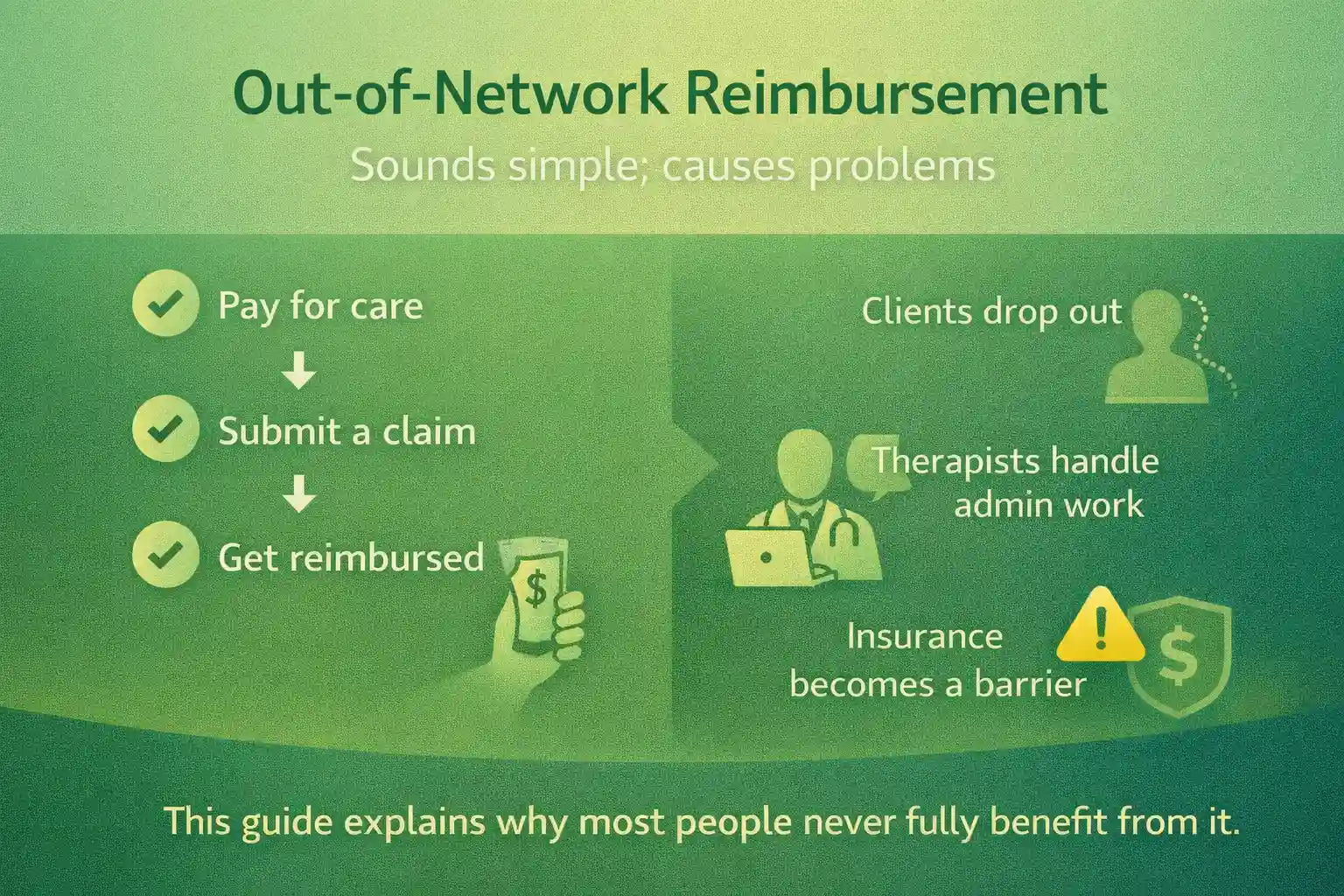

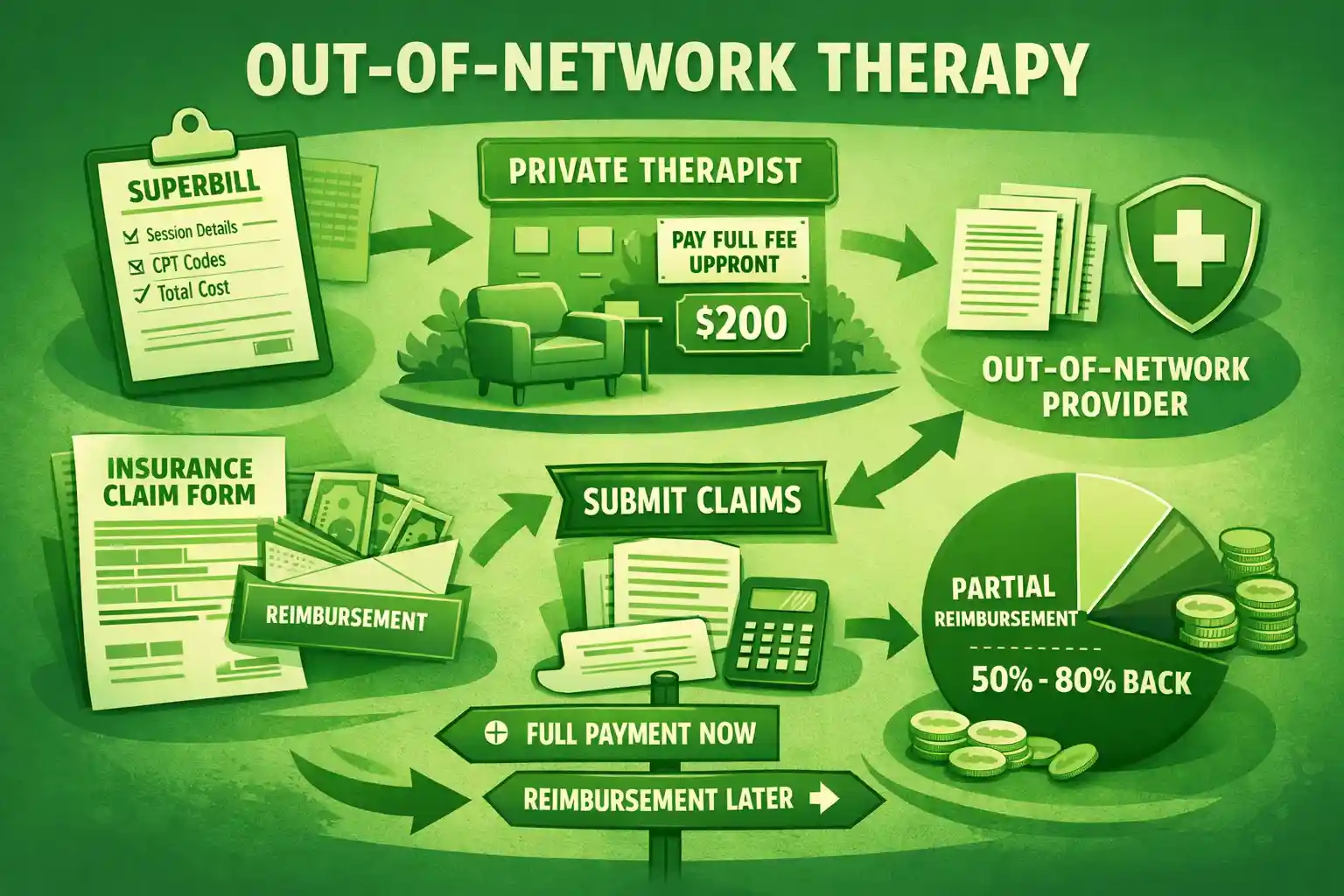

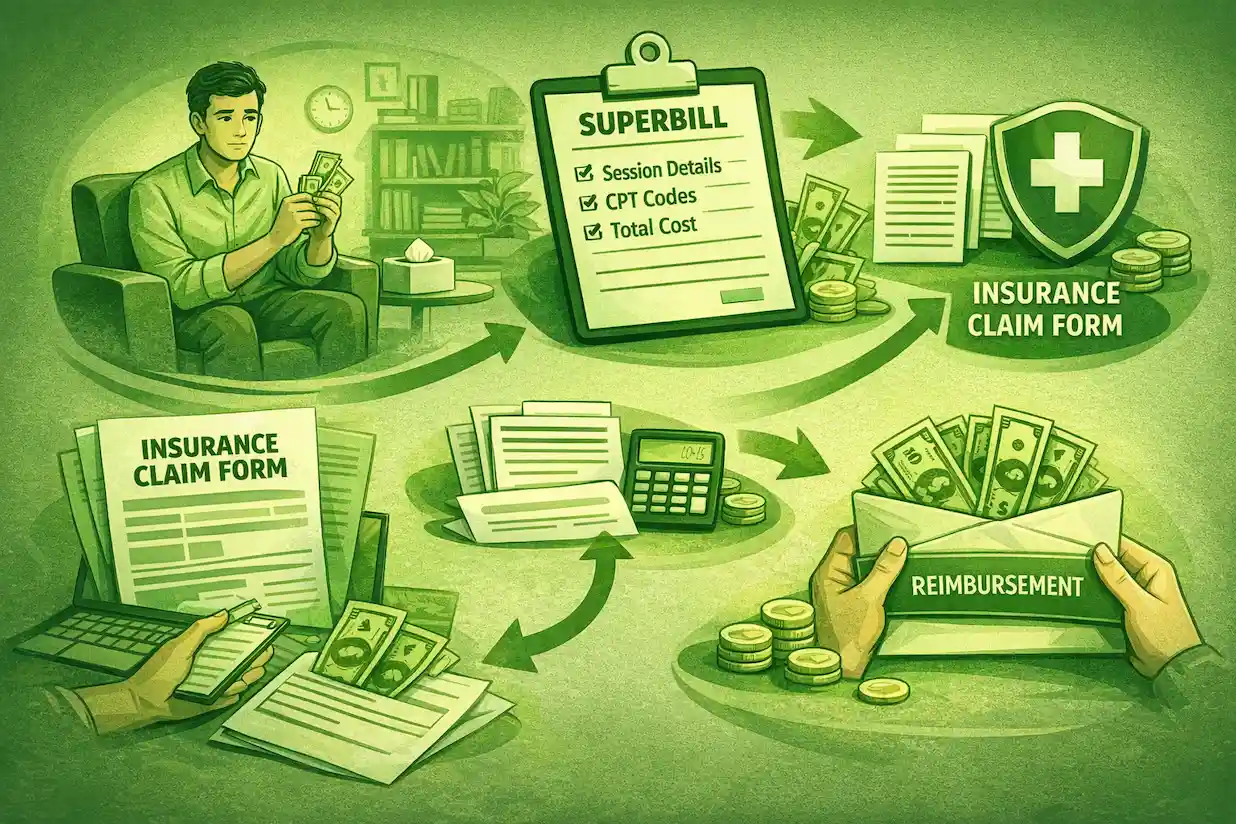

The Role of Out-of-Network Care

Another layer of complexity comes from provider networks. Many therapists choose not to contract with insurance companies, which means patients often end up paying out of pocket and seeking reimbursement afterward.

This isn’t necessarily a disadvantage, but it changes the financial flow.

Instead of paying a small copay upfront, you pay the full session fee and recover a portion later. Depending on your plan, reimbursement rates might fall between 50% and 80% of an allowed amount, which may or may not match what your therapist charges.

The process itself — submitting claims, understanding superbills, tracking reimbursements can be complex, especially if you’re unfamiliar with your medical billing rights.

If you’re navigating that side of the system, it helps to understand:

- How to get reimbursed for therapy

- What a superbill is and how it works

These aren’t edge cases; they’re becoming the default experience for many people seeking quality care.

What Therapy Actually Costs Over Time

When you zoom out, therapy pricing follows a pattern that most people aren’t shown upfront.

At the beginning, sessions often cost the full market rate, typically between $150 and $250 consistent with industry benchmarks for the average cost of therapy. After the deductible is met, that cost drops significantly, often into the $60 to $100 range depending on coinsurance. Eventually, if an out-of-pocket maximum is reached, additional sessions may be fully covered.

So the question isn’t just “how much does therapy cost,” but “when does it cost what.”

That timing difference is everything.

If you’re trying to estimate your own costs, the key variables are your session fee, your deductible, and your reimbursement rate. A structured estimate can make this much clearer:

👉 You can see your actual therapy cost based on your insurance using this calculator.

The Structural Problem No One Talks About

The issue isn’t that therapy isn’t covered. It’s that coverage is backloaded.

Insurance systems are designed around large, infrequent medical events. Therapy doesn’t fit that model. It’s ongoing, cumulative, and dependent on consistency. When the financial burden is concentrated at the beginning, it disrupts the very behavior the care depends on.

This is why dropout rates in therapy are highest early on. You can visualize this early drop-off pattern and how cost drives it here. It’s not just emotional resistance or lack of progress — it’s often financial friction.

You could think of it as a timing mismatch. The system provides support, but not at the moment when people need it most.

How to Approach Therapy Costs More Strategically

None of this means therapy is unaffordable. But it does mean it needs to be planned differently than most people expect.

Before starting, it’s worth understanding how quickly you’ll reach your deductible and what your per-session cost will look like afterward. If you’re already in therapy, tracking your cumulative spending can help you anticipate when that cost shift will happen.

For those using out-of-network providers, getting familiar with reimbursement mechanics can significantly reduce long-term costs, even if the upfront payments remain high.

A More Honest Way to Think About Coverage

Saying that therapy is “covered by insurance” isn’t wrong, but it’s incomplete.

A more accurate way to think about it is this:

Therapy becomes affordable over time — but requires upfront investment to get there.

Once you see the system this way, the pricing stops feeling arbitrary and starts becoming predictable. And with that predictability, it becomes easier to make decisions that align with both your financial reality and your care needs.

FAQ: Therapy Costs and Insurance

Why does therapy cost $200 even with insurance?

Even when therapy is covered, most insurance plans require you to pay the full session cost until you meet your deductible. This means you may pay $150–$250 per session upfront before insurance starts contributing.

How much does therapy cost with insurance after the deductible?

Once your deductible is met, therapy costs typically drop to $60–$100 per session, depending on your coinsurance or copay. The exact amount depends on your plan and whether your therapist is in-network.

Is it cheaper to go in-network or out-of-network for therapy?

In-network therapy usually has lower upfront costs (fixed copays), but fewer provider options. Out-of-network therapy often requires paying the full fee upfront, but you may get 50–80% reimbursed later, depending on your plan.

Why do people stop therapy early because of cost

Many people stop therapy before reaching their deductible, when sessions are most expensive. This early financial pressure creates a “drop-off” point where continuing care becomes difficult.

👉 You can explore how cost affects therapy retention over time here.