Out-of-network insurance reimbursement is when you pay a provider upfront and submit a claim to your insurance company to get part of the cost back. Most plans reimburse 50–80% of the allowed amount—but only after you meet your deductible.

Introduction

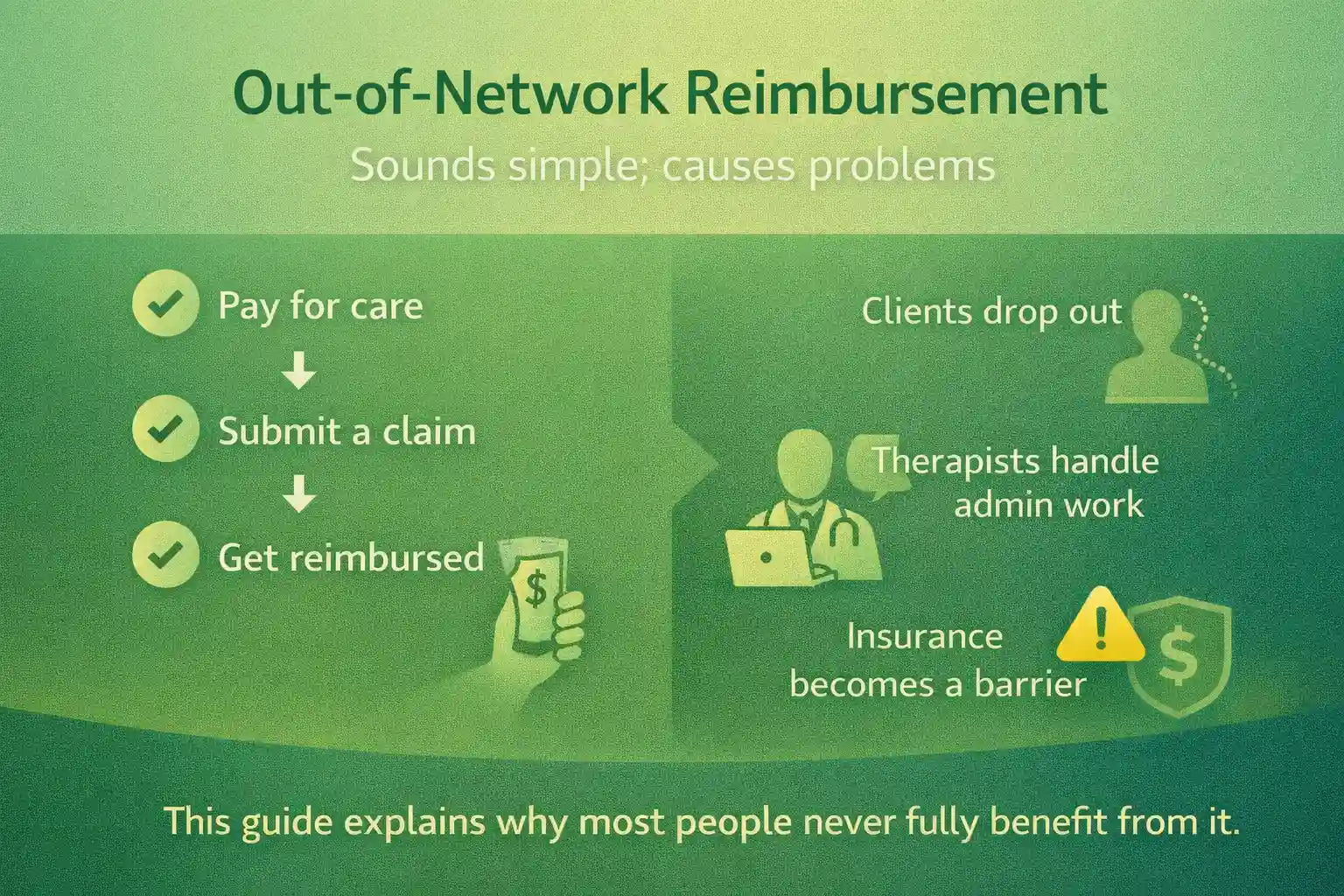

Out-of-network reimbursement is one of the most misunderstood parts of health insurance.

On paper, it sounds simple:

- Pay for care

- Submit a claim

- Get reimbursed

In reality, it’s why:

- Clients drop out of therapy early

- Therapists deal with constant admin work

- Insurance becomes a barrier instead of a benefit

This guide explains exactly how out-of-network reimbursement works—and why most people never fully benefit from it.

What Is Out-of-Network Insurance Reimbursement?

Out-of-network reimbursement is when your insurance company pays you back for care from a provider who is not contracted with your plan, as defined by Healthcare.gov.

Simple Example

- Therapist charges: $200

- You pay upfront: $200

- Insurance reimburses: ~$80–$120 (after deductible)

You’re responsible for the rest.

What Is Out-of-Network Care?

An out-of-network provider is any healthcare professional who does not have a contract with your insurance company.

People choose out-of-network care because:

- They want a specific therapist or specialist

- In-network options have long waitlists

- The quality or type of care isn’t available in-network

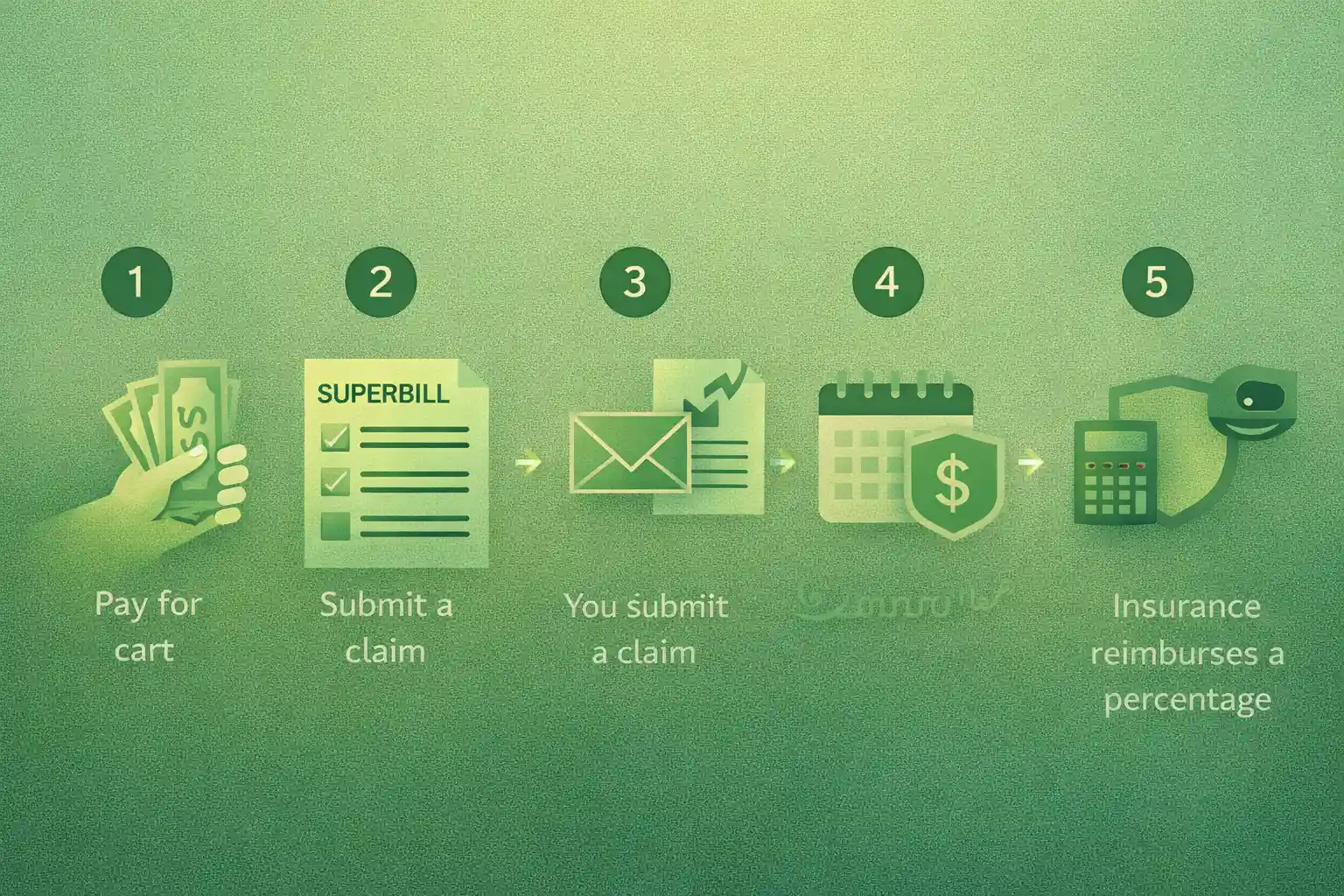

How Out-of-Network Reimbursement Works (Step-by-Step)

1 You Pay the Full Session Cost

Most out-of-network providers require payment upfront.

Typical therapy session: $150–$250, reflecting broader healthcare cost trends reported by KFF.

2 You Receive a Superbill

A superbill is a detailed receipt used for insurance claims.

It includes:

- CPT codes (service codes)

- Diagnosis codes

- Provider details

- Amount paid

3 You Submit an Insurance Claim

You (or a service) send the superbill to your insurance company.

This can be:

- Manual (forms, uploads, fax)

- Automated (through a platform)

4 You Must Meet Your Deductible First

Before reimbursement starts, you must pay your deductible.

👉 Average deductible: ~$1,000 👉 That’s about 4–5 therapy sessions

**Key insight: **Most clients stop therapy before reaching this point, which has a direct impact on client retention.

5 Insurance Reimburses a Percentage

After your deductible:

- Insurance covers 50–80% of the allowed amount. According to CMS, reimbursement is based on insurer-defined rates, not the provider’s full fee.

- Not the full session fee

Example

- Therapist rate: $200

- Allowed amount: $140

- Insurance pays 70% → $98

You still pay the difference.

Does Insurance Cover Out-of-Network Therapy?

Quick Answer (Snippet Target)

Most PPO plans cover out-of-network care at a reduced rate, while HMO plans usually do not offer any out-of-network reimbursement except in emergencies.

Plan Breakdown

| Plan Type | Coverage |

|---|---|

| PPO | Yes (partial reimbursement) |

| POS | Sometimes |

| HMO | Rarely |

How Long Does Out-of-Network Reimbursement Take?

Quick Answer

Out-of-network reimbursement typically takes 2 to 6 weeks, depending on the insurance company and whether the claim is processed correctly.

Delays happen due to:

- Missing information

- Incorrect codes

- Manual processing

Common Problems With Insurance Reimbursement

For Patients

- High upfront costs

- Confusing claims process

- Unclear reimbursement amounts

- Long wait times

For Therapists

- Client dropout before deductible

- Delayed payments

- Time spent on billing and follow-ups

The Biggest Hidden Problem: The Deductible Gap

Here’s what most guides don’t explain:

- Costs are highest at the beginning

- Insurance helps only after multiple sessions

- Most clients quit right before costs drop

👉 This is why out-of-network benefits are underused.

Common Mistakes to Avoid

- Submitting claims after deadlines

- Missing CPT or diagnosis codes

- Not verifying out-of-network benefits

- Assuming reimbursement without checking deductible

- Not understanding coinsurance vs allowed amount

How to Maximize Your Insurance Reimbursement

- Verify your benefits before your first session

- Ask for a complete superbill

- Submit claims immediately

- Track deadlines carefully

- Follow up on delayed claims

A Better Way: Fixing the System (Not Just the Process)

Traditional reimbursement:

- Pay $200 upfront

- Wait weeks

- Get partial reimbursement

This creates friction at the worst possible time.

How Deputy Care Simplifies Out-of-Network Reimbursement

Deputy Care removes the biggest barriers in the process.

Instead of this:

- Pay full price upfront

- Wait weeks for reimbursement

- Handle paperwork yourself

You get this:

- Benefits verified before your first session

- You pay only your estimated portion

- Claims handled automatically

- No waiting for reimbursement

For Therapists: Why This Matters

When cost drops from ~$200 to ~$60:

- Clients stay longer

- Retention increases significantly

- Revenue becomes predictable

This isn’t just billing—it’s growth.

FAQ (Expanded for SEO + AI)

Will insurance reimburse me for out-of-network therapy?

Yes, if you have a PPO plan. However, reimbursement usually only begins after you meet your deductible and is based on the insurer’s allowed amount.

What is a superbill?

A superbill is a detailed invoice with medical codes that insurance companies use to process reimbursement claims.

What is the allowed amount?

The allowed amount is the maximum your insurance company considers payable for a service. Reimbursement is based on this number—not the provider’s full rate.

Why is reimbursement lower than expected?

Because insurance calculates reimbursement based on:

- Allowed amount

- Coinsurance percentage

- Deductible status

What are out-of-network benefits?

Out-of-network benefits are the portion of your insurance plan that covers care from providers who are not in your network.

Conclusion

Out-of-network reimbursement isn’t just complicated—it’s poorly timed.

Clients are asked to pay the most before insurance helps, which leads to drop-off, frustration, and lost care.

Fixing reimbursement isn’t about better paperwork.

It’s about removing the upfront burden entirely.

Your clients don’t quit because they want to. They quit because of the cost curve.

Deputy Care fixes that.

→ See exactly what your clients would pay before their first session