Navigating the world of insurance can be daunting, especially for therapy practice owners. Understanding insurance terms is crucial for effective financial management. It can also enhance client retention and streamline operations.

Understanding insurance terms is crucial for effective financial management. Resources like Healthcare.gov glossary can help clarify common definitions used in health insurance. Insurance lingo often seems complex and overwhelming. Yet, mastering it can transform how you manage your practice. It can also improve your interactions with clients and insurers.

This guide aims to demystify common insurance terms and definitions. We will explore key concepts that impact your practice’s financial health. By the end, you’ll feel more confident in handling insurance-related matters. Insurance terms like premium, deductible, and copayment are fundamental. Knowing these can prevent unexpected costs and improve client satisfaction. They are the building blocks of effective practice management.

Health insurance lingo can be particularly tricky. However, breaking it down can aid in better decision-making. It empowers you to choose the right plans and negotiate better terms.

Understanding medical insurance terminology is vital for accurate billing. It reduces claim denials and enhances revenue cycle management. This knowledge is essential for maintaining a financially healthy practice.

Commercial insurance terminology is equally important. It helps in understanding business-related policies and planning for continuity. This ensures your practice is protected against unforeseen events.

In this article, we will provide a comprehensive glossary of insurance terms. Our goal is to equip you with the knowledge needed to navigate insurance complexities. This will ultimately lead to improved practice efficiency and client retention.

Why Knowing Insurance Terms Matters for Therapy Practices

Understanding insurance terms is not just beneficial; it’s essential for therapy practices. It streamlines financial processes, which is a significant advantage. When you’re clear about insurance language, your practice runs smoother.

Financial management is often a major struggle for many practice owners. Misunderstanding insurance terms can lead to billing errors and revenue loss. By mastering these terms, you reduce such risks considerably.

Insurance terminology affects every aspect of your practice. From client billing to reimbursement negotiations, these terms play crucial roles. Knowing them well enhances your operational efficiency.

Retention of clients is another critical area influenced by insurance literacy. Clients appreciate clarity about their financial obligations. When you explain insurance terms accurately, trust and satisfaction improve.

Here are some key benefits of understanding insurance terminology:

- Enhanced financial accuracy: Reduce claim denials and improve revenue.

- Improved client communication: Clearly convey costs and coverage details.

- Efficient operations: Streamline processes and reduce administrative burdens.

Therapists who can navigate insurance terms confidently make better business decisions. This knowledge empowers you to select suitable insurance plans for your practice. It also allows for effective negotiation of reimbursement rates.

Staying informed about insurance lingo also supports compliance. It ensures you adhere to industry regulations, thereby avoiding potential legal issues. Keeping up-to-date with evolving terminology strengthens your practice’s stability.

In conclusion, knowing insurance terms is a strategic advantage. It’s a way to protect your practice and support your clients better. With this knowledge, you can improve client relationships and practice efficiency.

The Basics: Key Insurance Terms Defined

Understanding the basics of insurance terms is your first step to better practice management. Let’s start with some common terms you will encounter. Many of these insurance terms are widely used across industries, as explained by Investopedia.

Premium is the amount you pay for insurance coverage. It’s usually paid monthly. Knowing your premium helps in budgeting and financial planning.

A Deductible refers to the amount paid out of pocket before insurance kicks in. This can greatly affect out-of-pocket costs for services.

Copayment is a fixed fee you pay for specific services. It’s usually small but adds up over time. Knowing copays can help clients prepare for appointments.

Coinsurance represents the percentage shared by the insured and insurer after the deductible is met. Unlike copayments, coinsurance is a percentage of the total cost.

The Explanation of Benefits (EOB) is a statement from the insurer. It details what was covered and what the patient owes. Understanding EOBs can prevent billing surprises.

Here’s a quick list of key insurance terms to remember:

- Premium: Monthly cost of insurance.

- Deductible: Out-of-pocket expenses before coverage.

- Copayment: Fixed fee for services.

- Coinsurance: Cost-sharing percentage.

- EOB: Statement of coverage details.

In-network providers are healthcare providers with agreements to offer services at reduced rates. This affects both cost and provider choice. It’s important to know which providers are in-network.

Out-of-network providers, on the other hand, may lead to higher costs. Out-of-network services can be expensive if not covered fully by your plan.

Pre-authorization is when certain services need approval by the insurer before they’re provided. This ensures the service qualifies for coverage.

Understanding these terms can significantly reduce unexpected costs. More importantly, it improves client satisfaction by clearly communicating what they need to pay.

Finally, clear communication about these insurance basics fosters trust. Clients are more likely to return when they fully understand their financial responsibilities.

Having a strong grasp of these basics sets the foundation for navigating more complex insurance topics. It ensures both practitioners and clients are on the same page. This shared understanding enhances the overall healthcare experience.

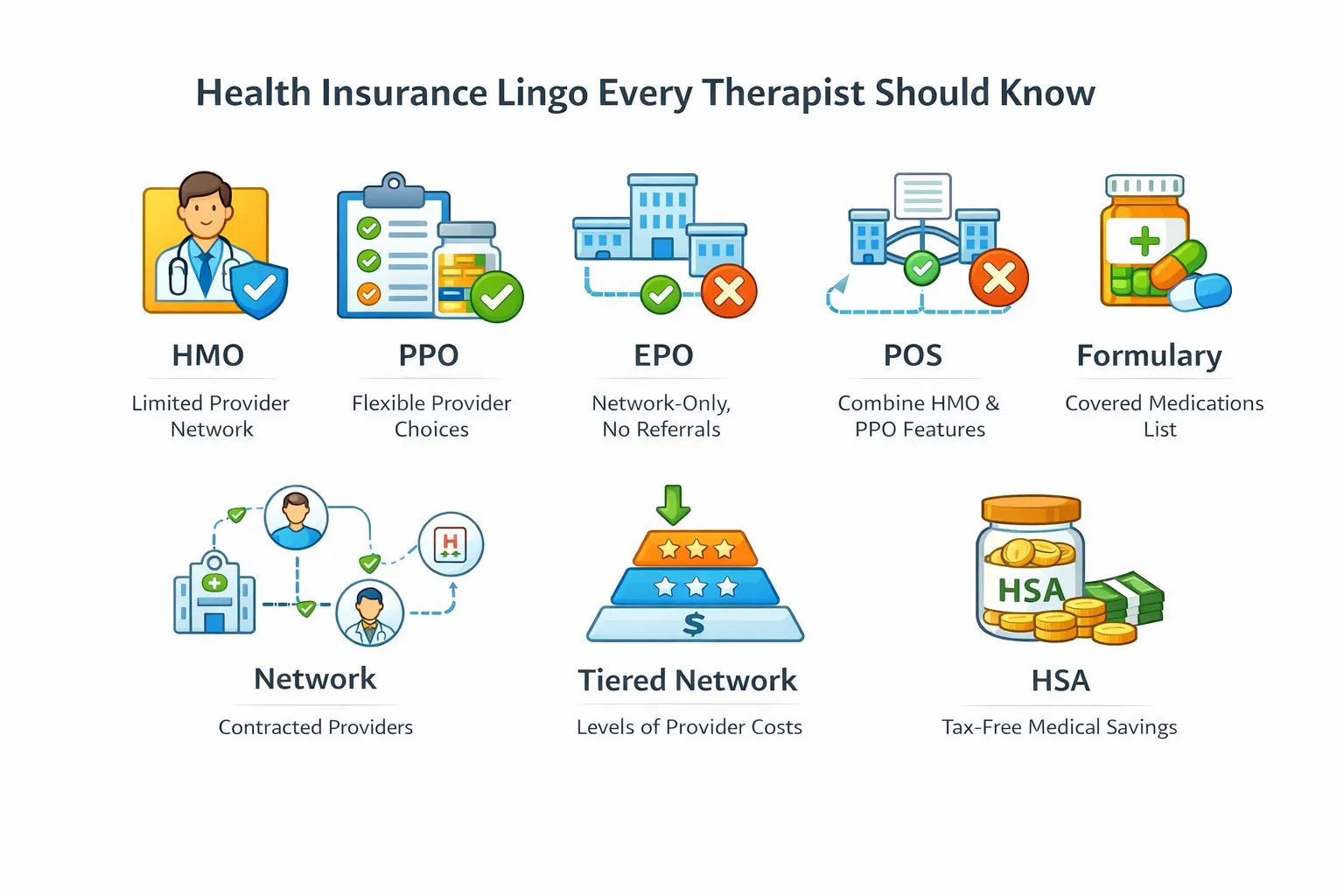

Health Insurance Lingo Every Therapist Should Know

Navigating health insurance lingo can feel daunting, but it’s crucial for effective practice management. Understanding these terms helps you assist clients effectively.

HMO (Health Maintenance Organization) plans often require clients to choose a primary care physician. It’s essential to understand how these plans limit provider networks. For therapists, knowing HMO restrictions helps guide clients in their choices.

PPO (Preferred Provider Organization) plans offer more flexibility in choosing providers. Clients can see out-of-network providers, though at a higher cost. This flexibility can impact clients’ decisions to continue therapy, affecting retention.

EPO (Exclusive Provider Organization) combines elements of HMO and PPO. Clients must use the plan’s network, like HMO, but without the need for referrals. It’s vital to know if therapists are part of these networks to provide options to clients.

POS (Point of Service) plans require clients to choose a primary care doctor from within the network. POS plans allow out-of-network visits but usually at a higher cost. Knowledge of POS structures aids in billing and client advisories.

Understanding Formulary lists is also essential. This list details which medications a health plan covers. Therapists should be aware of any medications their clients may be using and their coverage status.

Here’s a list of key health insurance lingo to know:

- HMO: Limited provider network.

- PPO: Flexible provider choices.

- EPO: Network-only without referrals.

- POS: Combines HMO and PPO features.

- Formulary: List of covered medications.

Network refers to the doctors, hospitals, and other healthcare providers who contract with a plan to provide services. Knowing if you’re in-network influences a client’s decision to choose your services.

Tiered Network is a system where different providers are grouped in levels. Clients pay more to use higher-tier providers. Awareness of tier systems can be a financial factor for clients attending therapy sessions.

Finally, Health Savings Accounts (HSAs) are tied to high-deductible insurance plans. HSAs allow clients to save money for medical expenses tax-free. Encouraging clients to utilize HSAs can make therapy more affordable.

Being familiar with these terms not only helps clarify billing processes but also enhances your role in supporting informed client decisions. It improves your ability to explain potential costs and coverage, contributing to a positive practice reputation. Understanding these insurances lingo facets streamlines operations, reduces miscommunications, and boosts client loyalty.

Medical Insurance Terminology: What Impacts Your Practice

Understanding medical insurance terminology is crucial for therapists. This knowledge aids in navigating billing, managing reimbursements, and advising clients on coverage options. For official definitions and policy-related terminology, refer to the CMS glossary.

Deductible is a fundamental term you must grasp. It refers to the amount a client pays out of pocket before insurance coverage kicks in. Knowing the deductible can help set realistic payment expectations for therapy sessions.

Then there’s Coinsurance, the percentage a client pays after the deductible is met. For example, with 20% coinsurance, the client pays 20% of costs while insurance covers 80%. Familiarity with coinsurance assists in accurate billing and cost discussions with clients.

A Copayment (or copay) is a fixed dollar amount the client pays for a service. It’s not affected by the deductible. Recognizing copay amounts ensures correct client invoices and reduces payment disputes.

Out-of-Pocket Maximum is another key concept. It caps what a client will spend on covered services in a year. Beyond this point, insurance covers 100% of costs. Understanding this helps when advising clients on long-term therapy plans.

An Explanation of Benefits (EOB) offers a detailed account of what the insurer covers after a claim is processed. Reviewing EOBs can reveal underpayments or corrections needed in your billing system.

Key medical insurance terms you need to know:

- Deductible: Upfront client payment.

- Coinsurance: Percentage costs shared post-deductible.

- Copayment: Fixed service fee.

- Out-of-Pocket Maximum: Annual spending limit.

- EOB: Coverage breakdown report.

Let’s not overlook Pre-authorization. This is when insurance requires approval before certain services are rendered. Being proactive in handling pre-authorizations avoids claim denials and ensures smoother billing processes.

Also, pay attention to Benefit Limits, which cap the total usage of covered services or financial limits per benefit period. Knowing these limits helps align treatment plans with financial coverage, preventing surprise expenses for clients.

Incorporating this detailed understanding of medical insurance terminology into your practice elevates client service. It minimizes confusion, streamlines billing, and enhances client retention by building trust and transparency. Clients, aware of their financial responsibilities, are more likely to commit to ongoing therapy, leading to better outcomes for them and stable revenue for you.

Commercial Insurance Terminology Glossary for Practice Owners

Navigating commercial insurance policies can feel daunting for practice owners. However, understanding key terms enables better decision-making and risk management.

Professional Liability Insurance, sometimes known as malpractice insurance, protects therapists against claims of negligence or inadequate performance. It’s an essential policy that shields your practice from legal and financial repercussions.

On the administrative side, be familiar with Policy Limit. This term defines the maximum amount an insurer will pay for a covered loss. Knowing this limit helps you assess whether current coverage adequately protects your practice.

Premium is another critical term. It’s the periodic payment required to keep the insurance policy active. By understanding premiums, you can budget more effectively and avoid lapses in coverage, ensuring continuous protection.

Next is Occurrence Coverage. It provides coverage for incidents that happen during the policy period, even if claims are filed later. This type of coverage ensures long-term protection from claims arising after policy expiration.

Claims-Made Coverage, in contrast, only covers claims filed during the active policy period. This coverage is usually less expensive but requires knowledge of its limitations, especially regarding retroactive coverage.

Add these commercial insurance terms to your glossary:

- Professional Liability Insurance: Malpractice protection.

- Policy Limit: Maximum claim payout.

- Premium: Cost of keeping coverage.

- Occurrence Coverage: Protection based on incident date.

- Claims-Made Coverage: Protection based on claim date.

Also important is Business Interruption Insurance. This type of policy covers lost income if your practice is disrupted by events like natural disasters. Understanding this option can assist in planning for unforeseen financial disruptions.

Lastly, consider Umbrella Insurance, which provides additional coverage beyond primary policy limits. It’s a smart choice for adding extra protection against significant claims, safeguarding your practice’s assets.

With these terms in your arsenal, you bolster your ability to manage risks and maintain financial stability. This knowledge translates into peace of mind, as you’re better equipped to protect your practice from common and uncommon risks alike.

Deep Dive: Terms in Insurance Policies That Affect Billing and Reimbursement

Understanding insurance policies is crucial for therapists concerned with billing and reimbursement. A strong grasp of specific terms can prevent financial setbacks and improve practice cash flow.

One fundamental term is Deductible. This is the amount a client pays out of pocket before insurance starts to cover expenses. In therapy, understanding each client’s deductible can help you set realistic billing expectations.

After the deductible is satisfied, Coinsurance becomes relevant. This is the shared cost between the client and the insurer. For example, a common coinsurance split is 80/20, where the insurer pays 80% and the client pays 20% of the remaining cost.

Another critical term, Copayment, refers to a fixed amount a client pays per visit. Unlike a deductible, copayments are required regardless of whether the deductible has been met. It’s essential to verify and communicate copayment amounts to clients to avoid billing disputes.

Consider these pivotal terms for your billing strategy:

- Deductible: Initial out-of-pocket client responsibility.

- Coinsurance: Shared post-deductible cost.

- Copayment: Fixed service fee per visit.

In-Network Provider is also significant. This term identifies providers who have agreements with insurers to offer services at reduced rates. Being in-network increases your visibility and can attract more clients whose plans provide better coverage for in-network services.

Conversely, an Out-of-Network Provider has no agreements with the insurer, usually resulting in higher costs for clients. Understanding the implications of being out-of-network can help you decide whether to pursue contracts with specific insurers.

Pre-authorization is another essential term. Some insurers require pre-authorization for certain types of therapy. This means obtaining insurer approval before treatment begins. Failing to secure pre-authorization can lead to denied claims, impacting your revenue.

Finally, always review the Explanation of Benefits (EOB) documents. These outlines what portion of the charges the insurance will cover, what the client owes, and any adjustments. EOBs help ensure that clients are billed correctly and that payments align with expected reimbursements.

Mastering these terms helps streamline billing processes, reducing errors and promoting better financial health for your practice. Understanding how these insurance terms influence reimbursement can lead to more accurate billing and enhanced client satisfaction.

Understanding Health Plan Terminology and Coverage Options

Grasping health plan terminology is vital for therapists aiming to optimize their service offerings and client satisfaction. Understanding coverage options can also help manage client expectations and practice revenues effectively.

At the core is the term Premium, which refers to the payment clients make to have insurance coverage. Typically paid monthly, this fee ensures access to healthcare benefits, including therapy sessions. Being aware of premium costs helps therapists anticipate the willingness of clients to seek additional services.

A pivotal concept is the Network. Insurance plans often categorize healthcare providers into network tiers. In-network services are those provided by healthcare professionals who have agreed to negotiated rates with the insurer, leading to lower costs for clients. This often influences a client’s choice of therapists.

In contrast, Out-of-network providers have no negotiated agreements, often resulting in higher charges for services rendered. It’s crucial for practices to communicate clearly about their network status to avoid unexpected costs for clients.

Consider these aspects when discussing coverage with clients:

- Premium: The monthly cost for coverage.

- Network: The tier of available providers.

- Benefits: The specific services covered.

The term Benefits refers to the range of services covered under a client’s health insurance plan. Benefits can vary, encompassing everything from counseling to specialized therapeutic services. Clarity on included benefits aids in precise service billing and reduces disputes.

It’s also important to understand Coverage Limits. These are the maximum amounts an insurer will pay for services within a policy period. Knowing these limits helps prevent surpassing coverage and aids in advising clients on potential out-of-pocket costs.

Lifetime Maximum is another term therapists should note. This represents the total amount the insurance will pay over the life of the policy. Once reached, coverage might cease, impacting long-term therapy plans and treatment continuity.

By understanding these health plan terminologies, therapists can offer informed guidance to clients, enhancing confidence in the service and ensuring financial transparency. Moreover, strategic knowledge of coverage options supports better management decisions, aligning services offered with client needs and insurance provisions.

Navigating Insurance Exclusions, Limitations, and Appeals

Insurance exclusions and limitations significantly affect financial transactions in therapy practices. Understanding these terms is crucial to avoid unexpected costs and ensure smooth operations. Exclusions are the specific services that an insurance policy explicitly does not cover. These often include experimental therapies or certain wellness programs. Knowing what’s excluded allows therapists to anticipate and inform clients ahead of any treatment plan.

Limitations, on the other hand, are constraints within covered services. These might encompass the number of therapy sessions allowed per year or restrictions on specific types of treatment. Being aware of these limits helps manage client expectations and prevents potential service denial.

Missteps often occur when therapists overlook policy exclusions and limitations. Hence, it’s vital to:

- Regularly review client insurance policies.

- Clarify any ambiguous terms with the insurer.

- Educate clients about potential out-of-pocket costs.

In cases where claims are denied, understanding the appeals process becomes paramount. An appeal is a formal request to an insurer to review a decision denying a benefit. Initiating an appeal requires thorough documentation and a clear rationale for why coverage should be granted. Familiarity with insurer procedures aids in preparing compelling appeals, increasing the likelihood of a favorable outcome.

Navigating these insurance aspects effectively reduces the risk of lost revenue and helps maintain client satisfaction. Regular communication with insurance representatives can also provide insights into common exclusions and the best strategies for handling them.

Therapists should also encourage clients to proactively understand their policies, promoting a collaborative approach to managing therapy costs. By mastering the intricacies of exclusions, limitations, and appeals, therapy practices can fortify their financial stability and trustworthiness, ultimately enhancing client loyalty and retention.

Insurance Acronyms and Industry Jargon Explained

Insurance jargon can be daunting, yet it’s essential for therapists to grasp to facilitate better practice management. Acronyms often simplify lengthy terms into digestible snippets, but they can be confusing without context. Understanding these acronyms and jargon helps demystify policies and enhances communication with insurers.

Commonly encountered acronyms in the insurance sector include:

- HMO (Health Maintenance Organization): A plan that requires members to use a network of specified doctors.

- PPO (Preferred Provider Organization): Offers more flexibility by allowing members to see out-of-network providers at a higher cost.

- EOB (Explanation of Benefits): A detailed statement from the insurer summarizing services received and the costs covered.

Insurance jargon often includes terms like “formularies,” which refer to lists of covered drugs, or “capitation,” a payment model where providers receive a set amount per patient regardless of services provided. These terms carry significant implications for billing and service delivery in a therapy practice.

Having a reference list of acronyms and jargon is beneficial. It allows therapists to quickly access critical information, ensuring clarity and informed decision-making. This proactive approach mitigates misunderstandings and enriches communication with both clients and insurance providers.

Developing proficiency in insurance terminology empowers therapists. It supports seamless interactions and builds trust with clients by explaining terms and their impact on therapy costs and options. Ultimately, this knowledge is a valuable asset, enhancing the practice’s operational efficiency and credibility.

How to Use an Insurance Glossary in Your Practice

An insurance glossary is a practical tool for therapists. It provides clear definitions of complex terms, fostering better understanding. This can improve the accuracy of billing and boost client satisfaction.

Incorporating a glossary into your practice involves several steps. First, create or find a comprehensive glossary that covers essential terms like premium, deductible, and copayment. Make sure it’s readily accessible for staff and clients.

Next, integrate the glossary into your client onboarding process. Explain key terms during initial consultations to enhance transparency. This proactive approach helps clients feel informed about their coverage and costs.

Use the glossary as a training resource for staff. Regularly reviewing terms ensures everyone in your practice is knowledgeable. This minimizes errors in billing and claims processing.

Finally, keep your glossary updated. Insurance industry terms can evolve, so periodically revise the glossary to reflect current language. This ensures your practice remains aligned with industry standards, contributing to smoother operations.

By utilizing an insurance glossary, therapists can demystify complex insurance language. This leads to improved communication with clients and insurers. It not only aids in financial management but also in building trust and enhancing client relationships within the practice.

Practical Strategies: Improving Client Retention Through Insurance Education

Educating clients on insurance can significantly boost retention. Educating clients on insurance can significantly boost client retention. When clients understand their insurance terms, they feel more valued and informed. This clarity builds trust and satisfaction, essential for long-term relationships.

The first strategy is to regularly host informational sessions. Offer workshops or webinars focusing on common insurance terms and policy explanations. These sessions give clients a comfortable environment to ask questions and gain insight.

Additionally, create easy-to-read educational materials. Use flyers, brochures, or digital content to explain key terms like coinsurance, out-of-network, and EOBs. Visual aids can simplify complex concepts, making them more approachable for clients.

Another effective method is personalized consultations. Incorporate insurance discussions into initial assessments and follow-ups. Tailor explanations to individual client situations, which shows personalized care and increases engagement.

Consider also developing a digital resource hub. A section on your website with frequently asked questions and an insurance glossary can serve as a valuable client reference. Being able to access information at any time empowers clients and reinforces their confidence in your practice.

Educating clients on insurance not only enhances their experience but also improves their overall satisfaction. These strategies foster transparency and reliability, which are key to improving client retention in therapy practices.

Frequently Asked Questions About Insurance Terms

Navigating insurance terminology can seem daunting. Here are some common questions therapists encounter about these terms.

1 What is the difference between a premium and a deductible?

The premium is the regular payment made to keep an insurance policy active. In contrast, a deductible is the amount paid out-of-pocket before insurance starts to cover costs.

2 How does coinsurance work?

Coinsurance is a cost-sharing structure between the insurer and insured. After the deductible is met, the insured pays a fixed percentage of covered expenses.

3 Why is an Explanation of Benefits (EOB) important?

An EOB outlines what an insurance plan covers and what costs the patient is responsible for after a claim is processed.

Here’s a quick list to clarify other common insurance questions:

- What is a copayment? A set fee for a specific service.

- What is pre-authorization? Prior approval for certain services.

- Who are in-network providers? Providers with agreements to lower service costs.

These FAQs provide clarity on insurance essentials. Understanding these concepts helps both therapists and clients manage expectations and avoid surprises. Always encourage clients to inquire about terms they don’t understand. This proactive approach can greatly enhance trust and efficacy in managing insurance within therapy practices.

Conclusion: Empowering Your Practice with Insurance Knowledge

Mastering insurance terminology is pivotal for successful practice management. It not only aids in financial clarity but also enhances client relations. Understanding these terms enables therapists to better handle billing and reduce claim denials.

Having a strong grasp of insurance language empowers therapists to negotiate reimbursement rates effectively. It simplifies explaining complex financial matters to clients, fostering trust and transparency. Clients appreciate when their therapists advocate for them with insurers.

Here are key benefits of insurance knowledge for your practice:

- Improved billing accuracy and reduced errors

- Enhanced client communication and trust

- Better strategic planning and financial management

Integrating insurance education into your practice can significantly impact client satisfaction and retention. By ensuring everyone in your practice understands these terms, you build a more efficient, reliable, and client-focused environment. This knowledge ultimately contributes to the growth and stability of your therapy practice. Embrace the potential that familiarity with insurance terms offers, and watch as both your practice and client relationships thrive.